- Not all assets go through probate; accounts with named beneficiaries transfer automatically, often causing confusion for the executor and the family.

- Institutions manage their own liability and privacy, meaning they usually will not disclose the name of a direct beneficiary to the executor.

- Your job is not to force disclosure or fix past paperwork, but to accurately document the transfer mechanism in your estate tracking logs.

- If a family member disputes a beneficiary designation (e.g., claiming undue influence), your role is to pause and consult an estate attorney, not to act as a judge.

- Always maintain a strict paper trail of your inquiries, even when an institution refuses to provide account details.

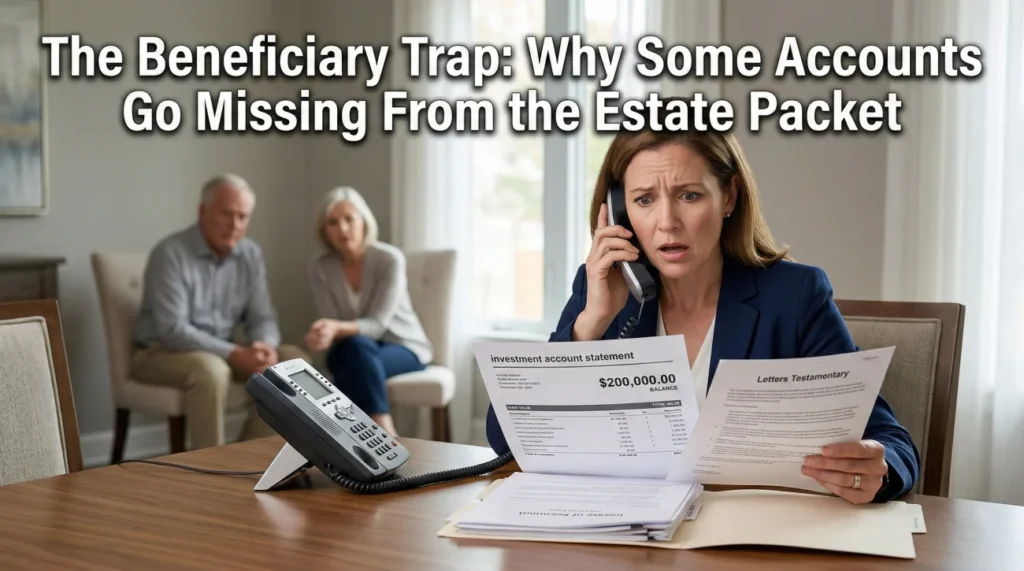

The $200,000 Surprise at the Dining Room Table

Last year, I helped an executor, we will call him David, who was organizing his late mother’s estate. The will was beautifully simple: everything was to be divided equally among David and his two younger sisters. David found a recent investment account statement showing a balance of nearly $200,000. He called the brokerage, provided his court-issued executor letters, and asked for the funds to be transferred into the estate account.

The representative placed him on a brief hold, came back, and politely informed him that the account was “handling itself.” It had a direct beneficiary named on file. Furthermore, due to privacy policies, they could not tell David who that beneficiary was. Two weeks later, David learned that his mother had updated the form years ago to leave the entire account solely to his youngest sister.

The fallout was immediate. The middle sister accused David of hiding assets. David felt completely blindsided by the institution. The entire probate process ground to a halt over a single piece of paperwork.

This is what I call the beneficiary trap. It is one of the most common friction points in estate administration. The shock comes from a fundamental misunderstanding: we are conditioned to believe that the will is the ultimate instruction manual for everything a person owned. In reality, modern financial systems rely heavily on direct contracts.

The Two Buckets of Estate Assets

To keep your sanity intact and communicate effectively with the family, you have to mentally divide the deceased person’s financial life into two distinct buckets. If you try to force everything into one bucket, you will be fighting a losing battle against institutional policy.

Bucket One: Probate Assets

These are the accounts and properties owned solely by the deceased person, with no attached instructions on what happens after death. Because there is no automatic instruction, these assets are essentially “frozen” until a court reviews the will and grants you the official authority to move them. As the executor, you manage these assets.

Bucket Two: Transfer-by-Contract Assets

Certain accounts have a built-in mechanism that triggers the moment the person passes away. Common examples include life insurance policies, retirement accounts, and standard bank accounts with a “Payable on Death” (POD) or “Transfer on Death” (TOD) designation attached.

When the account holder was alive, they signed a contract with the institution saying, “When I die, give this directly to this specific person.” That contract generally bypasses the will entirely. The institution is legally bound to follow that contract, and the asset never enters your jurisdiction as the executor.

An individual checking account with no named beneficiaries. The bank freezes it until you present court-issued authority to claim the funds for the estate.

An individual checking account with a Payable on Death designation. The bank bypasses you and releases funds directly to the named individual upon seeing the death certificate.

Understanding this distinction is critical when you are building your estate asset inventory checklist. If you do not tag the asset correctly in your master log, you will waste weeks trying to claim money that the estate has no legal right to touch.

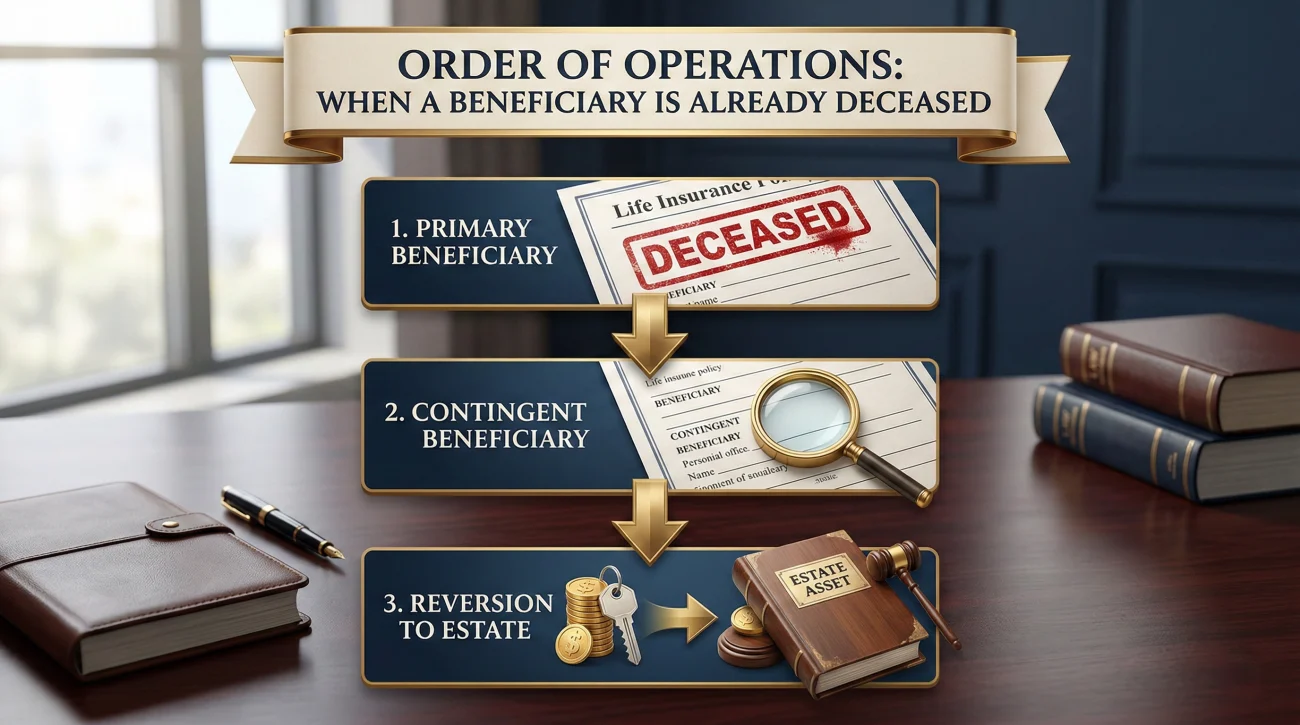

What If the Named Beneficiary Is Already Deceased?

The beneficiary trap gets slightly more complicated if the person named on the account passed away before the account holder. I see executors freeze when they uncover this scenario, unsure of who now owns the funds.

Institutions look at this in a strict order of operations:

- Primary Beneficiary: If they are deceased, the institution looks for a backup.

- Contingent Beneficiary: If the account holder named a secondary (contingent) beneficiary, the funds automatically route to them.

- Reversion to the Estate: If there are no living beneficiaries named on the form, the contract essentially “fails.” In most institutional frameworks, the funds then revert to the deceased person’s estate. At this exact moment, it transforms from Bucket Two (Contract Asset) into Bucket One (Probate Asset), and you, as the executor, finally have the authority to claim it.

Your action step here is not to guess. Your job is to provide the institution with the death certificates of both the account holder and the deceased beneficiary, and let their legal department determine the routing.

The Privacy Wall and the Reviewer’s Dilemma

The most frustrating part for an executor is not that the asset bypasses the estate, but that the institution often refuses to tell you who received it. You might ask, “Can you at least tell me who the beneficiary is so I can update the family?” and be met with a firm refusal.

Executors often take this personally, assuming the representative is being difficult. But if you look at it from the institution’s perspective, they are simply managing risk.

Key Point: Institutions view their relationship with the direct beneficiary as a strictly private matter. Unless the estate itself is the named beneficiary, the executor is legally considered a third party to that specific account.

Privacy policies dictate these rules. As noted in a MarketWatch Q&A regarding administrator access, financial institutions are protecting themselves from liability. If they disclose a name to you, and a family dispute erupts, the institution could be pulled into the crossfire. Furthermore, educational resources like Investopedia emphasize that beneficiary designations matter precisely because they are standalone, overriding contracts.

Pivoting the Conversation: How to Ask for Status

Because you cannot force them to break their privacy policy, continuing to demand a name will only result in a dead-end phone call. When you hit the privacy wall, your goal shifts: you no longer need the account details; you just need a clear, documented confirmation of the account’s status so you can prove to the family you did your job.

Script: Requesting Status Over the Phone

“I understand you cannot disclose the name of the beneficiary due to privacy policies. However, as the executor, I need to accurately complete my inventory of the estate’s assets. Can you simply confirm for my records whether this account has a direct beneficiary on file, and whether it will bypass the probate process entirely?”

Most representatives can answer a “yes or no” question about the mechanics of the account without violating privacy rules. Once they confirm it, you write it down, date it, and move on.

Setting Up Your Tracking Mechanism

A major part of communication hygiene is organizing your spreadsheets so they tell a clear story. If you cannot collect the funds, your log must reflect exactly why.

I always recommend creating a separate column in your master inventory specifically for “Transfer Mechanism.” This prevents you from staring at a blank space three months later, wondering why you never followed up on that life insurance policy.

| Institution | Account Type | Transfer Mechanism | Executor Action Taken |

|---|---|---|---|

| Institution A | Checking …4582 | Probate (No Beneficiary) | Mailed certified letters of authority on Oct 12. Pending response. |

| Institution B | Life Insurance Policy | Direct Beneficiary | Confirmed via phone Oct 14. Bypasses estate. Logged as closed for executor. |

| Institution C | Investment Account | Transfer on Death (TOD) | Institution confirmed TOD status Oct 15. Awaiting written confirmation letter. |

❌ Note: Never guess the beneficiary in your official logs. If the deceased person told you five years ago that their sibling was the beneficiary, do not write the sibling’s name in your log unless the institution explicitly confirms it. Paperwork changes. Document only what the institution verifies.

Building the Proof Trail for Unknowns

While the tracking spreadsheet organizes your workflow, it does not replace hard evidence. A common mistake executors make is spending hours trying to track down the beneficiary just to be helpful. While the impulse is kind, it is usually a poor use of your limited time.

If you know an account exists, but the institution will not give you details, you must build a “proof trail”—a chronological record proving you attempted to secure the asset, in case beneficiaries question your diligence later.

- 📄 Save the trigger document: If you found a statement in the mail, scan it. Name the file clearly:

2024-05-12_InstitutionX_Statement_FoundInMail.pdf. - ✅ Log the phone call: In your notebook, record the date, time, and the exact representative’s name who confirmed the account was a direct transfer.

- 📄 Request written confirmation: Ask the institution to mail a generic letter to the estate confirming that the account balance is zero for probate purposes, or that it was claimed by a designated beneficiary. They often have standard form letters for this.

Setting Expectations: What to Tell the Family

The operational problem of a missing account is easy to solve: you log it, build your proof trail, and move on. The human problem is much harder. Family members read the will, see that things are supposed to be split evenly, and then get angry when a large account is missing from the distribution.

Silence from the executor in this moment is dangerous. In my day-to-day admin work, I see that when executors fail to explain the concept of non-probate assets clearly and early, beneficiaries assume the executor is doing the math wrong.

The Proactive Update

You have to become an educator. Your job is to set the boundary early and show that your hands are tied by institutional policy, not by your own choices.

💡 Pro Tip: Address the concept of beneficiary accounts in your very first broad communication with the family. Plant the seed early so that if an account does bypass the estate later, it is not a shock.

Here is a copy-paste safe template you can adapt when you need to explain why an account is not in the final estate pool.

Subject: Status update regarding the estate inventory and non-probate accounts

Hello everyone,

I am writing to provide a quick update on the asset gathering process. I have been working with the various institutions to verify the accounts.

During this process, we have confirmed that certain accounts (such as the investment account at [Institution Name]) had direct beneficiary designations attached to them. As a standard rule, these accounts bypass the will entirely. The institution is required by their own contracts to transfer those funds directly to the individual named on their internal forms.

Because of strict privacy policies, the institution does not disclose the name of the beneficiary to the executor. They will reach out to the named individual directly.

I wanted to share this so everyone understands why this specific account will not be reflected in our final estate distribution. My authority as executor only covers accounts that do not have these direct instructions attached. I am continuing to consolidate the remaining estate assets and will keep you posted.

Best regards,

When to Step Back: Handling Family Disputes

Sometimes, communication is not enough. What happens if a family member receives your email and immediately replies, “Mom would never have left that account to John. He must have forced her to sign that form!”

This is where the beneficiary trap turns into a legal minefield. When allegations of “undue influence,” fraud, or diminished capacity arise regarding a beneficiary designation, the executor’s role is frequently misunderstood.

“Your job as executor is to manage the estate, not to act as a judge in family disputes over non-probate assets.”

If a serious dispute arises over a designation, do not attempt to mediate it yourself, and do not try to pressure the bank into changing their routing. Document the family member’s complaint in writing, maintain your neutrality, and immediately consult an estate litigation attorney. Disputes over non-probate contracts often occur outside the standard probate umbrella, and you need professional guidance to ensure you do not accidentally breach your fiduciary duty while trying to keep the peace.

Final Thoughts

Discovering that a major account is bypassing the estate can feel like a curveball. It disrupts your math and tests the patience of the family. The best way to navigate this trap is to rely on operational discipline rather than emotion.

Remember that your role is to administer the assets that legally fall under your jurisdiction, not to reverse-engineer the private contracts the deceased person signed years ago. By maintaining a meticulous tracking log, building a solid proof trail of your inquiries, and over-communicating the boundaries of your role to the beneficiaries, you protect yourself from unnecessary friction. When the institution says “no,” you simply write down the “no,” log the reason, and move forward.

Data and Sources

The operational guidelines in this article are supported by standard institutional practices and financial education resources:

- MarketWatch: Explainer on institutional privacy policies and why administrators are frequently denied beneficiary disclosure to limit liability. Read the Q&A here.

- Investopedia: Detailed breakdown of how and why beneficiary designations (Transfer on Death, Payable on Death) legally supersede instructions left in a will. Read the explainer here.

❓ FAQ

🎙️ Does a beneficiary designation override a will?

In most cases, yes. A direct designation is a binding contract with the financial institution, which legally takes precedence over instructions written in a will.

📞 Why won’t the bank tell me who the beneficiary is?

Banks are bound by privacy policies and risk management rules. Because the account bypasses the estate, the executor is treated as an unauthorized third party to that specific contract.

⏳ How long does a transfer on death take?

Unlike probate, which can take months or years, a TOD or POD transfer often happens within a few weeks once the named beneficiary submits their ID and the official death certificate.

📝 How do I list a beneficiary account on the estate inventory?

Log the account in your master spreadsheet to show you identified it, but mark the value as zero for the estate and note the mechanism as “Direct Beneficiary – Bypasses Estate.”

😡 What if my siblings want to sue over the beneficiary choice?

As the executor, you must remain neutral. If family members suspect fraud or undue influence regarding the designation, document their concerns and consult an estate litigation attorney immediately.

✉️ Will the bank mail statements for a TOD account to the executor?

Usually, no. Once the institution is notified of the death and verifies the TOD status, they typically freeze general correspondence and deal exclusively with the designated recipient.

📫 How does the beneficiary get notified?

While some institutions attempt to reach out if they have current contact info, it is typically up to the named beneficiary to proactively present their identification to claim the account.

🛑 Can a will change a life insurance beneficiary?

Generally, no. Changing a life insurance beneficiary requires submitting official update forms directly to the insurance company while the policyholder is still alive.

🤷♂️ What if the named beneficiary is already deceased?

The institution will look for a contingent (backup) beneficiary. If none exists, institutional policies usually dictate that the funds revert to the deceased person’s estate, becoming a probate asset.

📑 Do I still need the death certificate for beneficiary accounts?

Yes. Even though it bypasses probate, the institution requires an official death certificate to verify the passing before triggering the transfer.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.